It’s All About the Benjamins

How will the $150 billion industry evolve?

Disclaimer, NFA, all that legal stuff: All the information presented on this publication and its affiliates is strictly for educational purposes only. It should not be construed or taken as financial, legal, investment, or any other form of advice.

Hi folks 🙋🏻♂️,

Token2049 conference is happening in Singapore, so it has been a busy week. Apologies for the late issue. I’m not attending due to some personal matters, but the number of activities and energy is through the roof. Certainly one of the busiest times for crypto in Southeast Asia. From crazy crypto Twitter personalities walking around to the over-the-top Marina Bay Sands afterparties, it seems like the industry is very well capitalized. If the last sentence sounds like I’m FOMO-ing, trust your instinct.

It’s All About the Benjamins

Swiftly moving on, let’s talk stablecoins. As of September 2022, stablecoins account for ~15% of the entire crypto market cap, or roughly $150 billion. It’s heavily utilized by crypto market participants and has shown to have a brilliant product-market fit. In the bull cycle of 2017, stablecoins were barely there. They weren’t at the top of everybody’s mind as use cases were generally exchange-specific. Everything changed in early-mid 2020 when DeFi summer happened. Previously, there wasn’t any significant reason to utilize stablecoins if you were trading in a centralized exchange. Trades were settled off-chain and you could’ve easily cashed out to USD if you want to stay on the sidelines. Even in the derivatives market, traders would’ve done a 1x short BTC on BitMEX while holding spot BTC to stay neutral.

With the emergence of DeFi in 2020, on-chain markets infrastructure exponentially grew. Protocols such as Uniswap and Compound provided the necessary environment for stablecoins to find their product-market fit — starting the boom of their supplies.

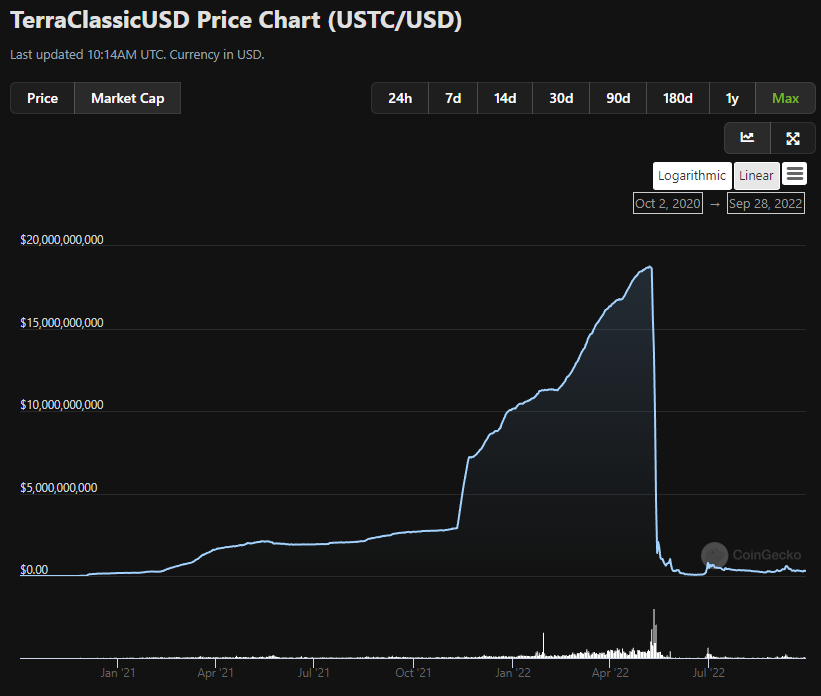

Not long after, industry participants realized the significance of having their own stablecoins and started a series of experiments to innovate on stablecoin models. The most notable one is Terra’s UST stablecoin, which had the brilliant idea to create an algorithmic stablecoin without any real collateral. The stablecoin is tied to the protocol’s native token, LUNA, and utilized a mint-and-burn mechanism to maintain the 1:1 peg with the USD. For a second, this seemed like a genius idea, combining the native token of the blockchain with smart contracts capability with a native stablecoin.

Surprise surprise.

UST imploded and lost ~$18 billion of its value overnight. To make things simple, this de-pegging event was caused by UST’s endogenous design. Endogenous basically means that the stablecoin is backed or partially backed by any tokens from the same issuer. Luca Prosperi, a researcher who’s active in the MakerDAO community, has previously written about this concept. In fact, the term endogenous is a critical language in the US House draft stablecoin bill, which we’ll unpack in this write-up. The future of this trillions dollar industry might have been changed forever.

Here are the quick takeaways:

The US stablecoin bill, if passed, will create a much more strict regulatory requirement, involving registration and banning endogenous collateralized stablecoins.

The important part is the registration aspect, which can create second-order effects for protocol-owned stablecoins.

A strong stablecoin industry will exacerbate the “dollar milkshake theory”.

It’s unrealistic to not expect any form of regulation, or expect lenient regulations, against stablecoins.

There will be a rise of non-USD peg stablecoins, that aim to stabilize value without pegging it to any FIAT currencies.

The Bill

The goal of the bill is to introduce a framework around stablecoin issuance. It covers the how and the who.

The “how” part dictates what type of stablecoins can be issued. Blame it on all Do Kwon. Under the new bill, there will be a 2-year ban on stablecoins that aren’t collateralized by cash or highly liquid assets, and issuing “endogenously collateralized” stablecoins will be punishable by crime. For existing stablecoins with the aforementioned model, there will be a 2-year grace period for the issuers to change their collateralization model.

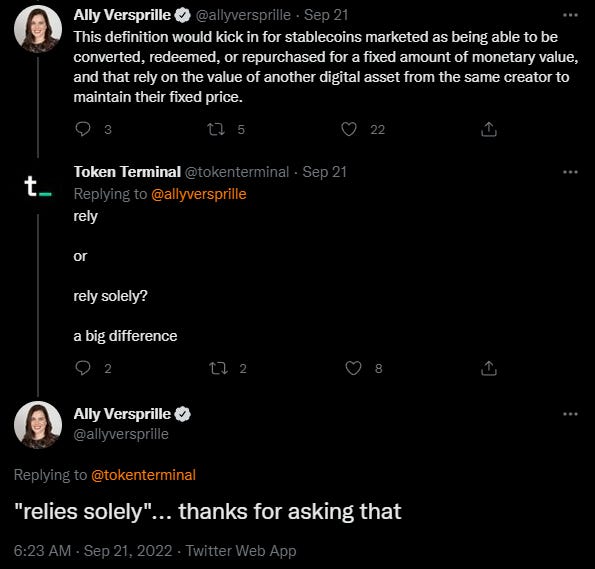

There’s more detail to be covered here as the bill moves forward in the process. A conversation on Twitter pointed out an interesting language difference. “Relies solely” means that Terra’s UST might not have been impacted by this bill, because it was partially backed by BTC at the very end of its life.

The “who” part dictates the necessary requirements for stablecoin issuers to comply with, and who will be regulating these issuers.

Nonbank issuers of stablecoins backed by fiat currency would also be overseen by state banking regulators and the Federal Reserve.

Banks or credit unions could issue their own stablecoins, which would be overseen by the Office of the Comptroller of the Currency and the Federal Deposit Insurance Corp.

Issuing a stablecoin without approval from those regulators could be punishable by up to five years in prison and a $1 million fine.

If passed, the requirement to receive approval can potentially create a lot more problems. It might directly disrupt DeFi’s composability. For instance:

if USDC has received approval from the appropriate regulators, does Compound need to receive the same approval for the protocol to issue cUSDC, a yield-bearing asset for its lending platform?

if I run a bridging protocol, do I need to receive approval for a bridged version of USDC?

if a wrapped version of stablecoin is necessary to connect with real-world assets, how would that play out?

You get the point. This bill can potentially create more uncertainties instead of providing a clear framework for industry participants.

Existing Stablecoins

How would this impact the top non-centralized stablecoins?

DAI

DAI is not backed by MKR, but MKR can be used as a last resort tool to cover the protocol’s deficit in the scenario that the Maker protocol is losing money.

This rarely happens, but it has happened before.

The bill shouldn’t impact MKR.

FRAX

FRAX is partially backed by FXS, which is FRAX’s governance token.

The collateral ratio of FXS will update depending on the utilization rate of FRAX.

The bill will put FRAX under scrutiny as it is partially endogenously collateralized by a token from the same issuer.

LUSD

LUSD is not backed by LQTY, which is LUSD’s governance token.

LUSD is primarily backed by ETH.

The bill shouldn’t impact LUSD.

USDD

USDD is partially backed by TRX, which is endogenous to the USDD ecosystem.

USDD is ~30%+ backed by TRX.

The bill will put USDD under scrutiny as it is partially endogenously collateralized by a token from the same issuer.

USDN

USDN is backed by WAVES, which is endogenous to the USDN ecosystem.

The bill will put USDN under scrutiny as it is partially endogenously collateralized by a token from the same issuer.

MIM

MIM is not backed by SPELL, which is MIM’s governance token.

MIM is backed by other assets, primarily FTT.

The bill shouldn’t impact MIM.

I believe that we’ll see a rise of non-USD peg stablecoins, that aim to stabilize value without pegging it to any FIAT currencies. However, it’s very unlikely for these types of stablecoins to reach mainstream adoption. Don’t get me wrong, I haven’t given up on these concepts (e.g. RAI), but there’s a lot of work to be done to scale it and make it user-friendly for non-crypto native consumers. I have a few ideas, but that’s for another post.

Pragmatism

Aligning with the spirit of this publication, I think it’s unrealistic to expect no regulation or lenient regulation towards stablecoins. Despite the rise of libertarian tech bro public figures, we still live in a society where governments govern. Stablecoins are directly tied to FIAT currencies, which are a tool of governance and stability for governments around the world. That’s why even countries with amazing economic growth over the past few decades such as South Korea still implement some form of capital control.

Even in the scenario that the US let the stablecoin industry flourishes and exacerbate the dollar milkshake theory, non-US jurisdiction won’t stay put and let their currencies weaken. I’m a believer of the dollar milkshake theory, but it’s naive to expect that other FIAT currencies will go down without a fight.

Alas, we’ll see increasing regulations in the stablecoin landscape. Industry participants need to draw from both spectrums. Be pragmatic and adapt to the situation, while actively championing friendlier regulations through various measures. No matter what happens, the stablecoin industry will still be worth in the trillions, it’s not a matter of when, but a matter of how.

Life & Work

Being in your mid-20s is the best and weirdest feeling at the same time. In your early 20s, pretty much all of your peers are working towards their professional goals. People talk about work and how to make more money. But in your mid to late 20s, people start to diverge. You see those who are more ambitious than ever to have a FatFire lifestyle, those who become digital nomads in Bali doing e-Commerce dropshipping, and those that have settled down with children. I still don’t know where exactly I fall; but a few days ago, a friend of mine wrote a brilliant piece about the contemporary state of work. In his piece, he hypothesized that there are two types of people. For type 1, work brings joy to their lives and it’s their Ikigai. For type 2, work is an evil necessity to ensure livelihood. All that I know is that I’m grateful to have found the crypto space — this crazy whacky world is indeed my Ikigai.

Until next time,

Marco M.